Accelerating the Gulf's Energy Transition in the Wake of Russia's War

The Russian war against Ukraine has been both a gift and a curse for oil producers in the Persian Gulf. It has stoked oil demand, but also made clear the strategic necessity of the energy transition.

This article is part of a series exploring regional energy cooperation in the Gulf and is published in cooperation with Istituto Affari Internazionali.

The 2022 Russian war against Ukraine has been both a gift and a curse for oil producers in the Persian Gulf. In the short term, the war has created restraint for the development of renewables, contributed to the high oil demand, and in doing so demonstrated the need for more international investment in oil exploration and drilling. High oil prices and the resulting profits enabled the member states of the Gulf Cooperation Council (GCC) to partially offset financial losses from previous years—and also benefitted the economies of these member states. However, the transition to a new model of global energy consumption has not been cancelled—it has only been delayed.

This conflict clearly demonstrated the economic risk of excessive dependence on hydrocarbon-based resources, and as a result the leading GCC countries began to develop clear action plans for speeding up the energy transition. For the Gulf’s traditional oil producers, this is a huge challenge: after the short hiatus forced by the war, the race to switch to renewable energy will restart and force the Gulf states to once again work against time to prepare the oil sector for the “post-oil” era.

In general, most GCC states base their current strategy on an understanding of two contradictory but coexisting trends in the global energy market—trends created by the war in Ukraine. The first relates to national security issues: individual countries may find it necessary to extend their hydrocarbon use. The second and conflicting trend is that some players may accelerate their transition to renewables for the same security considerations and to reduce their dependence on fluctuating hydrocarbon prices.

Economic Development and Political Considerations

If the GCC countries are to reduce their current economic dependence on hydrocarbon exports, they need to diversify on a large scale into renewable energies. Alongside this, there is a need to maximise income from oil exports—something which can be achieved by simultaneously reducing domestic consumption and increasing oil output. However, GCC members will need to avoid increasing the volume of CO2 emissions, as these damage the health of the population and cause environmental damage.

But the political considerations are tied to the rentier social contract model of the states in the GCC. This model is now becoming too costly; budgets are uncertain against a backdrop of fluctuating oil prices. The fourth energy transition—and related processes, such as decarbonisation, digitalisation, and the development of renewable and alternative energy sources—will enable Gulf states to generate additional sources of income to finance government subsidies and social programmes. The development of the renewables sector will additionally contribute to preserving the social contract, provided that its growth will also lead to the provision of new and high-paying jobs for the citizens in the public sector.

External Influences

Other countries are placing increasing pressure on GCC states to accelerate their energy transition—and to make the oil they export more environmentally friendly (a marketing requirement formulated by the global push for energy transition). To maintain the competitiveness of their oil in the global market, Gulf producers are forced to take steps to reduce the environmental harm that can be caused by the production and transportation of hydrocarbons. The active spread beyond the United States and the European Union (including in Asian countries, who have been the traditional sales market for the GCC countries) of what some term the “green agenda” further increases the importance of presenting hydrocarbon products as green and minimising the negative impact on the environment.

Moreover, GCC countries will inevitably be pressured by the international community to implement international climate agreements. In 2022, the Arab states took an active part in the COP 27 climate summit in Egypt, and again in 2023, when they held the COP 28 summit in the UAE. The latter was a major milestone: its final document not only summed up what the international community had done within the framework of the Paris Agreement, but also recognised the need to phase out energy derived from fossil fuels. In light of these developments, by early 2024, almost all GCC states had put forward their own net-zero emissions targets.

Circular Carbon Economy

It is important to note that the final COP 28 document calls for a gradual phase-out of the use of oil in energy systems but emphasises that this process should be carried out without prejudice to hydrocarbon producers. This duality fully meets the needs of the Persian Gulf countries. They are ready to provide consumers with hydrocarbons for as long as they are needed—for example, the European Union, which seeks greater independence from Russian supplies—and cooperate with the international community in preparing for a “post-oil” world. Under these circumstances, most GCC states now speak not only about the need to increase the proportion of energy generated by renewables, but also about the goal of creating a special form of the Gulf’s circular economy that could still be built on the base of the region’s hydrocarbon riches.

Thus, the so-called circular carbon economy concept promoted by Saudi Arabia does not reject the further development of oil and petrochemical industries of the Kingdom but implies the introduction of obligatory compensation measures for emissions through the active use of carbon capture technologies (CCUS). It also argues about the increased role of renewable energy sources in the production and transportation of hydrocarbons. Alongside these plans, the Gulf countries are also developing a strategy to become world-leading hydrogen producers.

Options for Cooperation

In Iran, deteriorating climatic conditions and attendant ecological problems are creating extra incentives for the government to increase its efforts to make the energy transition and restructure its economy. In a sense, the country started investigating ways to develop its own renewable sector long before the idea became popular among its neighbours. Possessing substantial hydro, wind, and solar energy-producing potential, Iran achieved substantial progress in developing these in 2000–2010. Unfortunately, any further progress was substantially slowed and in some areas even prevented by the sanctions placed on the country from 2010 onwards, although by 2022 Iran was still among the top five countries in the Middle East in terms of how much electricity is generated by renewables. Its experience in the renewables development field can still be of interest to other Gulf countries, and Tehran itself can learn a lot from the GCC member states about the use of CCUS technologies and renewables in the production and transportation of hydrocarbons.

The current situation might intensify levels of cooperation among the Gulf countries, and also between these countries and international partners. There is a good incentive to cooperate—between both the Gulf players within OPEC and those on the bilateral track—as the GCC economies and oil sectors will have a lot of challenges in common that they need to prepare for. Meanwhile, the Gulf states need to ensure a stable and long-term demand for Gulf hydrocarbons, which means regional players must invest more in Asian economies and attract Asian investments. Moreover, an important element of the Gulf countries’ economic strategies is now to attract and allocate in-house and international investments in both the traditional and renewable energy sectors.

Alongside other developments, the war in Ukraine has led to a clear intensification of European diplomacy in the Gulf and a revision of some past practices. Traditionally, European concerns about Gulf domestic policies limited the interaction between EU countries and GCC states in the energy field, but many of these concerns have been pushed aside. Instead, the European Union has demonstrated its readiness to help the GCC countries in their own transition to renewable energy sources, making it clear that it expects the Gulf to help the EU move away from its dependence on Russia’s oil and gas and ease the influence of geopolitical factors on oil prices.

Road Ahead

It is worth noting that the GCC countries do not intend to entirely replace the hydrocarbon sector with renewable energy production or to phase out oil usage or the development of petrochemicals. Instead, the Gulf states see the sustainable energy sector (as well as those industries accompanying the fourth energy transition) as a complement and addition to their hydrocarbon-based economies. The wealth they have accrued through hydrocarbons will allow them to accelerate diversification and make the “old” oil industry look eco-friendly. None of the Gulf states has abandoned plans to develop petrochemical production, seeing in it an opportunity to conveniently and easily diversify GCC economies and as a response to the question of what to do when oil is not in demand as feedstock for fuel production. As oil market analyst Tsvetana Paraskova puts it: “Renewable energy could replace more and more fossil fuels in power generation and transportation, but these are not the only industries using oil and gas. From medicines to cosmetics, clothing, and technology, the world will still need oil.” This is well understood in the Persian Gulf, and the various crises have shown that fluctuations in demand for hydrocarbons have not always depended on the demand for fuel.

In the medium and long term, adaptation to a new energy order would require Persian Gulf oil producers to restructure their economies and revise their social contracts to withstand a decline in demand and a reduction in prices for oil resources. They would need to rebuild their energy systems for a lower-carbon future while simultaneously ensuring the survival of their oil industries. Moreover, the Gulf states clearly understand the need to adapt to the growth of competition in traditional markets, particularly in Asia, and will need to consider multilateral cooperation to offset some challenges.

Looking into the future, the hydrocarbon production and petrochemical sectors will remain the backbone of the Gulf countries’ economic structure. The main motivations that shape the development plans in the region are twofold: to increase sources of income through diversification, including the development of hydrogen exports; and to ensure the profitability of the traditional oil sector for as long as possible. The likely success factors in this quest will be the reduction of the cost of producing both hydrocarbon-based and sustainable energy, the reduction of harmful emissions from traditional industries, and the maintenance of the necessary level of investment in both the oil sector and the new energy sources. As UAE Minister of Energy and Industry Suhail Mohammed Almazroui succinctly put it, “drop the cost, drop the carbon, maintain the investment.”

Photo: Dubai Protocol Department

EU Embargo of Russian Oil Spells Trouble for Iran

European Union leaders have agreed on a landmark embargo of Russian oil that will seek to slash imports by 90 percent by the end of the year. That is bad news for Iran.

European Union leaders have agreed on a landmark embargo of Russian oil that will seek to slash imports by 90 percent by the end of the year. The embargo represents a major intensification of European sanctions on Russia following the invasion of Ukraine.

For most oil producers, the embargo will be a boon. While the measures were widely expected and therefore may have been partly priced-in by traders, oil prices jumped on the news. Saudi Arabia, for one, is already planning how it will spend the windfall enabled by high oil prices.

But for Iran, and to a lesser extent Venezuela, the embargo of Russian oil is bad news. For countries whose oil exports are subject to U.S. or EU sanctions, China is the buyer of last resort. For several years, China has been the sole country to continue significant purchases Iranian and Venezuelan crude oil, ignoring the threat of U.S. secondary sanctions. These imports have been an important contributor to Iran’s economic resilience under sanctions. However, this is not because revenues are flowing back to Iran. The revenues accruing in China are being used to sustain Iran’s imports of crucial intermediate goods for the country’s manufacturing base.

Iran has also benefited from increased financial resources in the United Arab Emirates and Malaysia, two countries which are serving to intermediate Chinese imports of Iranian oil. Most Iranian oil arriving in China is declared as an import from the UAE or Malaysia. As it stands, Iran is consistently exporting more than 1 million barrels per day of crude oil to China.

Russia’s rise as a major energy exporter to China corresponds to the period in which Iranian oil was taken off the market due to the impacts of US, EU, and UN sanctions programmes—Iran’s demise as an oil exporter helped open the door for Russian exports.

The new EU embargo on Russian oil will intensify competition between Russia and Iran in China’s oil market. Russian suppliers are already offering buyers a 30 percent discount on benchmark prices, a much steeper discount than Iran has offered Chinese buyers in recent years. Russia and Iran will be competing for the business of the limited number of Chinese refiners willing to process “sanctioned” oil.

Already, some Chinese “teapot” refiners are replacing Iranian oil with Russian oil because of the attractive discounts on offer. So far, customs data does not reflect a dramatic swing away from Iranian imports. But it is early days and the embargo will dramatically change incentives. According to the IEA, around “60 percent of Russia’s oil exports go to OECD Europe, and another 20 percent go to China.” While some customers, such as India, might import the Russian barrels that would have otherwise gone to Europe, political and economic realities will require Russia to push more oil into the Chinese market.

Looking to Chinese customs data for April, Russia’s ability to squeeze Iran becomes clear. It is clearly a more important supplier of crude oil to China. While logistical bottlenecks might prevent an immediate jump in Chinese purchases, all of the Russian barrels already flowing to China are newly subject to discounts—China can insist on lower prices now that the EU embargo is in place. This in turn creates pressure for Iran to match Russian discounts or risk losing market share.

While it is possible that the further pressure on global supply might push oil prices even higher, minimising the loss of revenue for Iran even as Chinese imports fall, in the medium term, Russia has the means to bully Iran due to its lower fiscal breakeven price and lower production costs. At the outset of the COVID-19 pandemic, Vladimir Putin boasted that Russia could withstand oil prices of as low as $25 dollars per barrel for as long as a decade. Iran’s oil sector, already weakened by a decade of sanctions, does not have the same ability to endure low prices. In short, Russia can afford to undercut Iran.

Plus, for whatever period that Russian oil is not subject to U.S. secondary sanctions, Chinese tankers and refiners may prefer to handle Russian crude, due to the lower risk of enforcement action.

Iran has a couple of options here. First, it could try and negotiate an arrangement with Russia, agreeing not to engage in a race to the bottom when it comes to pricing their sanctioned barrels for China. Iran might even be able to play a role as an intermediary in Russian energy exports to China, importing refined products across the Caspian and exporting crude oil to China as part of a swap arrangement. But this kind of cooperation is highly unlikely given the track record of Russia-Iran relations and the fact that Russia sees Iran as the junior partner in the relationship.

The second option would be for Iran to try and get itself out of this predicament by taking decisive steps to restore the nuclear deal. Doing so would see the rollback of U.S. secondary sanctions on Iranian oil and enable the resumption of exports to European buyers precisely when those buyers need it most. Earlier this month, EU High Representative Josep Borrell commented on the heightened value of the nuclear deal for Europe in the wake of the Russia crisis. He told the Financial Times that “Europeans will be very much beneficiaries from this deal” as the “the situation has changed now.” He added that “it would be very much interesting for us to have another [crude] supplier.”

Earlier this week, Iranian officials boasted that oil revenues were up 60 percent year-on-year owing to the high oil prices. But the situation has changed now. As the EU moves forward with its historic embargo, Iran’s oil revenues are suddenly in Russian crosshairs.

Photo: Kremlin.ru

Concern in Iran Over China Commerce as Trump Gets Trade Deal

The contents of an email shared with Bourse & Bazaar by an official at Iran’s communications ministry suggest that China’s Bank of Kunlun is weighing whether to cease processing Iran-related payments. There is growing concern in Tehran that China may be planning to downgrade its trade relationship with Iran.

Last week, an official from Iran’s communications ministry received an email from a Chinese supplier informing them that Bank of Kunlun, the state-owned bank at the heart of China-Iran bilateral trade, is weighing whether to cease processing Iran-related payments.

The email warned that after an April 9 deadline, “Kunlun may stop handling payment [sic] from Iran. For the exact situation then, we can only wait for further notice from the bank.”

The bank was set to inform clients that “all the payment [sic] should be received and goods should be shipped before April 9, and all PI (pro forma invoice) dates should be before January 10.”

The official, who shared the contents of the email with Bourse & Bazaar on condition of anonymity, speculated that the change in policy at Bank of Kunlun could be related to the recent agreement reached between Chinese and American negotiators over the first phase of a new trade deal.

If the email proves accurate, this would not be the first time that Kunlun has suddenly changed its policy in response to political developments in Washington. The bank paused its Iran business for one-month period following the Trump administration’s reimposition of secondary sanctions on Iran in November 2018. When Iran transactions were resumed, a new policy limited payments for trade in “humanitarian and non-sanctioned goods and services between Iran and China,” minimizing direct contravention of U.S. sanctions.

Reached for comment, Wu Peimin, the economic counselor at the Chinese embassy in Tehran, stated the embassy had not been made aware of any impending change in policy at Kunlun and that concerns amount to a “hypothetical situation.”

As analysts Julia Gurol and Jacopo Scita detail in a recent report, China’s has continued to purchase Iranian oil in defiance of U.S. sanctions in an “attempt to appease Iran and avoid a full-scale conflict in the Persian Gulf.” Although China has rebalanced its imports in favor of Saudi Arabia and could easily find an alternative supplier for the low volumes of oil still imported from Iran, recent incidents such as the attack on the Aramco facilities in Abqaiq and Khurais have made clear the risks to Chinese energy security if Iran acts on threats to prevent all exports through the Strait of Hormuz in the event it is prevented from exporting its oil.

But while China’s strategic interests are well-served by maintaining trade ties with Iran, albeit at reduced levels, there remains the possibility that China may have made tactical concessions related to Iran as part of its trade negotiations with the United States. For their side, U.S. officials have insisted that they would not reduce sanctions pressure on Chinese firms trading with Iran in order to gain concessions from Beijing related to the trade deal.

Chinese trade with Iran has fallen due to sanctions pressures, but remains a pillar of Iran’s economic resiliency in the face of the Trump administration’s “maximum pressure” sanctions campaign. Iran’s bilateral trade with China totaled USD 23 billion last year. While the annual total has fallen 34.5 percent, Iran has sustained significant oil and non-oil exports to China, totaling just over USD 13.2 billion dollars. The earnings from this trade have enabled Iran to afford continued imports of Chinese raw materials, parts, and machinery that support Iran’s manufacturing sector—total imports were USD 9.7 billion in 2019.

Much of this trade was facilitated through the payment channels available at Kunlun, a so-called “bad bank” sanctioned by the United States in 2012 for its critical role in supporting Chinese trade with Iran, particularly oil purchases by major state refiners like CNPC and Sinopec.

Mohammad Reza Karbasi, who is responsible for international affairs at the Iran Chamber of Commerce, expressed confidence that even if Kunlun proceeds to eliminate its Iran business, other smaller Chinese banks will step-in to support the longstanding bilateral trade between China and Iran.

“Iran is important to China and the same is true the other way round as well. Sure, there are attempts by Western governments to try and interfere with the expansion of ties between us, but we believe the Chinese won’t let them succeed given the trust that has been built between our two counties through years of cooperation,” Karbasi said.

In a recent interview focused on the trade deal, Treasury Secretary Steven Mnuchin stated that the Trump administration was “working closely with [China] to make sure that they cease all additional activities [with Iran]." The Trump administration has continued to sanction Chinese firms engaged in Iran trade, most recently targeting several buyers of Iranian oil.

Mnuchin also stated that “China state companies are not buying oil from Iran.” The statement remains factually incorrect—Chinese firms such as CNPC remain directly engaged in Iran oil purchases—but it may refer to a new understanding between China and the United States that is yet to be implemented.

Richard Nephew, who led sanctions policy at the State Department during the Obama administration, recently told S&P Platts that he does not expect such designations and the related pressure to compel China to drop it’s Iran trade outright.

However, reports that Iran’s January oil exports are significantly higher than the monthly average since May 2019 may reflect stockpiling of cheap Iranian oil by Chinese refiners ahead of an expected change in policy and reduction in imports. A similar pattern was observed when exports peaked in March 2019 ahead of the May 2019 revocation of the waiver permitting Chinese purchases of Iranian oil.

Given the timing, concerns in Tehran center on whether China will further downgrade its trade with Iran in order to avoid jeopardizing its new understanding with the Trump administration on larger issues of economic policy.

Massoud Maleki, the director of the Bureau for Developing Countries at the Tehran Chamber of Commerce said he was skeptical of reports Kunlun would bring an end to its Iran business, but warned of the consequences if there were such disruptions.

“Iran and China’s trade is not a paltry amount for it to be carried out through suitcase trade or exchange bureaus. If this is true, then I’m afraid that we will have to deal with a whole lot of hardship. This, I presume, is unlikely, but if it’s confirmed we must prepare and take necessary measures,” said Maleki.

Farhad Ehteshamzad, an Iranian industrialist and former head of Iran Auto Importers Association, echoed the call for preparations in case the U.S.-China trade deal has changed China’s intentions regarding trade with Iran.

“Transactions through the Bank of Kunlun had already been made difficult during the past two or three months. Kunlun in China was like one of our small credit institutions in Iran before being trusted with the responsibility to handle Iran payments. It gets all its reputation via collaboration with Iranian businesses.’

He added that if the industry ministry official had received such an email, the Central Bank of Iran has also been forewarned and urged officials to ensure that the Iranian funds currently held in accounts at Kunlun are not blocked.

“An emergency meeting should be held to determine how much capital lies in the bank and to inform traders and economic players before their money gets blocked. Also, if there is the possibility for certain goods to be shipped before April 9, this has to be done. If there isn’t, then money has to be transferred from Kunlun bank to other banks as quickly as possible before the money is out of reach.”

Ehteshamzad estimates that around 80 percent of payments made to support China-Iran bilateral trade are currently processed via Kunlun. “Yet, this does not mean if the bank stops its services, trade will come to a halt,” he insisted.

Citing the creativity and resolve of Iran’s private sector, Ehteshamzad noted that Iranian business boast “a myriad ways to circumnavigate the U.S. sanctions. The only downside to this is that transaction costs will rise, meaning goods will take longer to be delivered and will cost more.”

For now, Iran’s business community is waiting nervously to see whether decisions made in Washington and Beijing will force them to put their creative powers to use once again.

Photo: U.S. Embassy Beijing

China’s Declared Imports of Iranian Oil Hit a (Deceptive) New Low

◢ New data from China’s customs administration show a significant drop in purchases of Iranian oil. The declared value of September imports was just USD 254 million, down 34 percent from August and down 80 percent from the same month last year. But observed exports from Iran remain high, suggesting that the customs data is not capturing the full value of Iranian oil sales to China.

New data from China’s customs administration show a significant drop in purchases of Iranian oil. The declared value of September imports was just USD 254 million, down 34 percent from August and down 80 percent from the same month last year.

The September data appears to end a period of relative stability for Chinese imports of Iranian oil following the Trump administration’s revocation of a key sanctions waiver in May, since when China has continued to purchase Iranian oil in direct violation of U.S. sanctions.

But the decline in purchases of Iranian oil was not matched by a decline in Chinese purchases of non-oil goods. Non-oil imports from Iran exceeded USD 500 million in September, a level of monthly trade that has remained stable since April of this year and which is consistent with the monthly average observed over the last two years.

This suggests that the fluctuation in oil purchases is not related to a system-wide disruption in China-Iran trade such as the banking difficulties that stymied commerce late last year. Additionally, Chinese exports to Iran did not decline month-on-month in September.

According to data provided by TankerTrackers.com, fewer barrels of oil were observed departing Iran in August than in July. Observed exports amounted to around 670,000 bpd in August, down by about 130,000 bpd from the previous month. This drop in observed exports offers one explanation as to why Chinese declared imports of Iranian oil were lower in September than in August—export levels in a given month tend to appear as declared imports in the following month given the four week journey of tankers at sea.

Notably, any decision to scale back imports of Iranian oil in September would have predated the Trump administration’s move to sanction tanker subsidiaries of Chinese state shipping giant COSCO involved in the transport of Iranian oil. The Chinese government has reportedly asked the Trump administration to remove sanctions on COSCO as part of its ongoing trade negotiations.

In July, U.S. officials had publicly expressed concern about continued Chinese purchases of Iranian oil, suggesting that China was given prior warning that its tanker fleet could be targeted with sanctions designations. This may have spurred China to reduce the use of its own VLCC tankers in the transport of Iranian oil. The fleet of the National Iranian Tanker Company (NITC) has long been the primary means by which Iranian oil is exported to China, but having fewer Chinese tankers picking up oil from terminals in Iran would nonetheless reduce export capacity, depressing overall imports.

However, data on observed exports from Iran does not correspond to the drop in declared imports in September’s customs data. The value of the observed exports is considerably higher than the USD 250 million in Chinese purchases declared for September. The market value of Iran’s August exports is over USD 1.2 billion. Syria is the only other customer currently purchasing Iranian oil and imports significantly less than China. So where is the additional oil going?

Some tankers which departed Iran for China in August are still in transit, waiting for ship-to-ship transfers that will take the Iranian crude to its final port destination. Other tankers may have delivered their oil into bonded storage, meaning that the oil has not yet been sold to China and is therefore not captured in the customs data.

But the most obvious explanation for why declared imports lag observed exports is actually captured in the customs data—just not in the entry for Iran. Reports earlier this summer noted ship-to-ship transfer activity off the coast of Malaysia that appeared to be tied to exports from Iran. Chinese customs data from the last few months illustrates how the drop declared imports from Iran is concurrent with a marked increase in imports from Malaysia.

Since May of this year, Malaysia has exported an average of USD 1.2 billion worth of oil to China each month. The monthly average in the twelve months leading up to May was just USD 1 billion. Re-export of Iranian oil via Malaysia allows China to overcome the capacity problem introduced by the threat of sanctions on major players like COSCO. China can use smaller tankers for the final leg of the journey from Iran, picking up oil from Iranian VLCCs.

Looking ahead, TankerTrackers.com has reported total Iranian exports of around 485,000 bpd in September, a decline of 185,000 bpd when compared to the previous month. With less crude at sea, the value of oil imports declared in China’s October customs data may even fall below the September level. Yet there is little evidence that China is making a strategic decision to further decrease imports of Iranian oil. On the contrary, the strategy to sustain a baseline of imports appears to be growing more sophisticated.

Photo: Depositphoto

Here’s What the French Proposal for Trump and Iran Actually Entails

◢ A new report in the Daily Beast claims that Trump is flirting with a “$15 billion bailout for Iran.” But the mechanics of the proposal Trump is considering, put forward by French President Emmanuel Macron, are far more limited and reasonable than this and other reports have suggested.

A new report in the Daily Beast exclaims that Trump is flirting with a “$15 billion bailout for Iran.” But the mechanics of the proposal Trump is considering, put forward by French President Emmanuel Macron, are far more limited and reasonable than this and other reports may have you believe. What is being deliberated is a plan that does nothing more than restore Iran economic benefits it was already receiving under the Joint Comprehensive Plan of Action (JCPOA), until Trump withdrew from the agreement, reinstating U.S. secondary sanctions.

Back in 2017, French, Italian, and Spanish refiners were importing around 600,000 bpd of Iranian oil on an annual basis. When the U.S. reimposed sanctions on Iran in November of 2018, it provided waivers for eight of Iran’s oil customers to sustain their imports at limited volumes. Italy was the only European customer to receive a waiver, but given the complicated nature of U.S. sanctions, the waiver itself was insufficient to give Italian state oil company ENI enough comfort to continue buying Iranian oil.

Eventually, in May of 2019, the oil waivers were fully eliminated, causing Iran’s oil exports to plummet further. Only China and Syria continue to buy Iranian oil in defiance of US sanctions. The cessation of European imports of Iranian oil has been the single greatest source of frustration for Iranian policymakers, who feel that Europe is failing to keep up its end of the bargain under the JCPOA nuclear deal. Iran imports a large volume of machinery and medicines from Europe—the loss of euro denominated revenues makes it much harder and more expensive for Iran to sustain these crucial imports, putting a strain on the Iranian economy.

In the face of these challenges, Europe established INSTEX, a state owned trade intermediary that would allow trade in non-sanctioned goods to flow without the need for cross-border financial transactions, and by extension, Iranian use of its now precious reserves of euros. But INSTEX has been hampered by the fact that it offers Iran no solution to sustain its oil sales to Europe. Not only is Iran ceding market share, but in its current form INSTEX will be unable to facilitate the billions of euros worth of imports from Europe that are currently left vulnerable without Iranian oil being sold to Europe in tandem.

This is the problem the French proposal seeks to solve. It is basically a riff on a proposal first put forward by the Iranians. The Iranians argued that if Europe is unable to purchase Iranian oil due to the reticence of European tanker companies and refiners to handle the crude, then Iran should “pre-sell” oil to Europe. Iran would be provided a line of credit today guaranteed against future oil sales to Europe to be completed when sanctions relief allows.

The figure that has been associated with the French plan—$15 billion—is a direct reflection of what it would take for Europe to restore the financial component of their oil purchases under the JCPOA. Over the course of a year, the value of 700,000 bpd in oil exports at a price of $58 per barrel is approximately $15 billion dollars. For context, in 2017, Europe imported 29,035,298 metric tonnes of crude oil, which is the equivalent of approximately 583,092 bpd. At the then still low oil prices, the value of those imports was just over EUR 10 billion. Accounting for a higher oil price and the need for round numbers, a $15 billion commitment is reflective of a normal state of affairs for European purchases of Iranian oil.

In short, the French are not aiming to provide any new money to Iran. Their plan is designed to provide Iran a financial benefit it was already receiving—in accordance with US sanctions relief—back in 2017. In this sense, the French are merely seeking permission from the Trump administration to restore their own compliance with the implementation of economic benefits of the JCPOA—a request growing more urgent as Iran loosens its own compliance with its nuclear commitments under the deal.

In some respects it is surprising that the French would embrace this plan given their relatively tepid push to sustain the economic benefits of the deal for Iran to date. But it would appear that President Macron believes a more substantial move is necessary to bring about a “ceasefire” in the economic war waged by Trump, and the Iranian escalations being pursued in response.

Crucially, the French plan does not call upon the U.S. to lend a single cent to Iran. The reason the Macron has appealed to Trump reflects both the political reality that he needs to de-escalate tensions between the U.S. and Iran as well as the practical reality that Europe is unable to provide the envisioned financial support without a sanctions waiver from the Treasury Department, either for the credit line itself, or for resumed oil sales.

The creation of new credit facilities for Iran was actually first considered in the summer of 2018 prior to the creation of INSTEX. European central banks were asked to consider opening a direct financial channel to Iran’s central bank to ease payment difficulties and enable the provision of export credit. But the central banks balked at the idea, both because Iran has yet to fully implement the financial crime regulations required by its FATF action plan (reforms which have still not been fully implemented) and also because of concerns about U.S. retaliation. Close advisors to the Trump administration were publicly calling for European central bankers to be sanctioned if such faculties were extended to Iran.

So some consent from the U.S. will be required to operationalized the French proposal. That may irk the Iranians, but it also makes the plan more feasible. European and Iranian policy makers alike have been disabused of the idea that direct defiance of U.S. sanctions is possible for France and the other EU member states. Macron has therefore decided to try and coax Trump towards a negotiated solution, dangling in front of him the prospect of talks with Iranian President Hassan Rouhani.

But importantly, the U.S. would be making a minimal concession to secure such talks. Any waiver granted to the Europeans could be revoked and the financial benefit Iran would receive is only part of the full financial benefits they were receiving prior to Trump’s withdrawal from the JCPOA and the reimposition of U.S. secondary sanctions.

Photo: Wikicommons

China Takes More Iranian Oil, Intensifying Sanctions Challenge

◢ China has taken its second Iranian cargo of crude oil after US waivers expired in early May, further defying US sanctions on Iran’s oil exports. The HORSE, a VLCC owned by the National Iranian Tanker Company (NITC) discharged its oil at Tianjin port in northern China, data provided by market intelligence firm Kpler shows.

China has taken its second Iranian cargo of crude oil after US waivers expired in early May, further defying sanctions on Iran’s oil exports. The HORSE, a VLCC owned by the National Iranian Tanker Company (NITC) discharged its oil at Tianjin port in northern China, data provided by market intelligence firm Kpler shows. The crude could be destined to Sinopec’s Tianjin refinery. This comes ten days after Iran’s first shipment of oil to the CNPC-operated Jinxi refinery, previously reported by Bourse & Bazaar.

Senior analyst Homayoun Falakhsahi shared Kpler’s analysis: “The HORSE arrived at Tianjin on 29 May and discharged 2.12 million barrels of crude oil it had loaded from Iran’s Kharg Island on May 6th. After its departure from Kharg the following day, the cargo went offline for a few weeks before reappearing passing Singapore on its way towards China.”

In the past, HORSE has delivered crude and condensate to refineries in China and India. The tanker’s latest voyage provides further confirmation that China has restarted importing Iranian oil after a brief pause following the expiration of US waivers. Due to their significant exposure to the US financial system, state oil companies CNPC and Sinopec had initially ceased importing Iranian oil in May, citing the risk of sanctions penalties.

China, traditionally Iran’s largest oil customer, holds the key to the future of the country’s oil exports. Under the 6-month waiver period, China imported 600 kbd of crude and condensate on average from Iran, 43 percent of the country’s oil exports in the period.

In the run-up to the revocation of the waivers, China’s imports from Iran reached an all-time high of 913 kbd in April before decreasing to 299 kbd in May, when the final vessels to have departed Iran before the waiver revocation arrived in port. Against the backdrop of the trade war with the US, Beijing now appears to be undermining Washington’s goal of bringing Iran’s oil exports down to zero. Kpler data suggests that Chinese imports in June currently total 186 kbd, including two cargoes that left Iran before May 2nd.

The resumed imports reflect state policy. “The fact that state-owned CNPC and possibly Sinopec have restarted taking Iran’s oil indicates Beijing has given the green light to do so,” said Falakshahi. China has an interest in receiving Iranian oil not just for its energy security, but also because of outstanding debts owed by Iran. Around 100 kbd of Iran’s oil to China is used by the National Iranian Oil Company in repayment of costs and remuneration for Chinese investment in the country’s upstream oil and gas sector. In the last decade, CNPC and Sinopec invested a total of $3.8 billion in the Azadegan North and Yadavaran oil fields respectively, two of Iran’s West Karun projects.

Since the revocation of US sanctions waivers, Iran has struggled to find a home for its oil. Iranian oil minister Bijan Zanganeh has said that the oil export situation is much worse than during the Iran-Iraq War, noting, “We can’t sell our oil under Iran’s name”. Shipments of oil have slumped from 1.32 mbd in April to 984 kbd in May and 515 kbd in June.

However, as much as 75 percent of these exports could reflect Iran’s recourse to floating storage as wells continue to pump more oil than buyers are willing to take. Aside from China, the other traditional buyers of Iranian oil—India, Turkey, Japan and South Korea—have fully halted their imports so far, though India says it is considering importing Iranian oil again. Iran will be hoping it’s other customers are inspired to follow China’s lead.

Photo: Shana.ir

Iran Completes Delivery of First Chinese Oil Purchase Since May

◢ According to analysis provided by TankerTrackers.com, a tanker owned by the National Iranian Tanker Company (NITC) has delivered oil to the Jinxi Refining and Chemical Complex in China, marking the first confirmed delivery of Iranian crude purchased after the Trump administration’s revocation of waivers permitting the sale of Iranian oil on May 2.

A tanker owned by the National Iranian Tanker Company (NITC) has delivered oil to the Jinxi Refining and Chemical Complex in China, marking the first confirmed delivery of Iranian crude purchased after the Trump administration’s revocation of waivers permitting the sale of Iranian oil on May 2.

Analysis provided by TankerTrackers.com shows that the medium-sized Suezmax vessel, named SALINA, departed from Iran’s Kharg Island terminal on May 24. SALINA loaded approximately one million barrels of Iranian oil before departing on May 28.

A few weeks later, on June 20, the vessel arrived at the Jinxi Refinery, located near the Port of Jinzhou, near Beijing. Notably, Jinxi is owned and operated by PetroChina, which is affiliated to China National Petroleum Corporation (CNPC), a long-time buyer of Iranian oil and the parent company of Bank of Kunlun, the financial institution that has been at the heart of China-Iran trade for the last decade.

Iran has been delivering significant volumes of crude oil into bonded storage in China over the last year, selling that oil to China in subsequent months. CNPC’s nearby storage facility—part of China’s Strategic Petroleum Reserve—can hold 19 million barrels. But in the absence of waivers, the storage of Iranian oil would still contravene US sanctions, making it likely that the delivered oil was taken by CNPC as a purchase.

SALINA’s journey serves to confirm earlier reports that China had resumed purchasing Iranian petroleum products, including crude oil and liquid petroleum gas, despite the fact that such purchases would run afoul of US sanctions. Several other tankers are expected to arrive in China in the coming weeks.

The central role of state-owned CNPC, China’s second largest energy conglomerate, suggests that China has resumed purchases of Iranian oil as a matter of government policy. During a visit to Beijing in May, Iranian foreign minister Javad Zarif was reassured by his Chinese counterpart, Wang Yi, that China would continue to support Iran, so long as Iran remained in compliance with the Joint Comprehensive Plan of Action (JCPOA) nuclear deal. However, Chinese and Iranian officials continue to deny that any purchases have been made since May, preferring to maintain ambiguity over the exports.

The Chinese General Administration of Customs declared USD 585 million in imports of Iranian petroleum products in May, down sharply from USD 1.6 billion in April. But imports are expected to rebound in June, based on the significant number of tankers that remain en route to Chinese ports.

Photo: Justo Prieto

China Restarts Purchases of Iranian Oil, Bucking Trump’s Sanctions

◢ On the same day that Iranian foreign minister Javad Zarif traveled to Beijing for talks on "regional and international issues,” the Chinese oil tanker PACIFIC BRAVO began to head east, having loaded approximately 2 million barrels of Iranian oil from the Soroosh and Kharg terminals in the Persian Gulf over the past few days, according to analysis provided by TankerTrackers.com.

On the same day that Iranian foreign minister Javad Zarif traveled to Beijing for talks on "regional and international issues,” the Chinese oil tanker PACIFIC BRAVO began traveling eastward, having loaded approximately 2 million barrels of Iranian oil from the Soroosh and Kharg terminals in the Persian Gulf over the past few days, according to analysis provided by TankerTrackers.com.

PACIFIC BRAVO is currently reporting its destination as Indonesia, but the tanker was recently acquired by Bank of Kunlun, a financial institution that is owned by the Chinese state oil company CNPC. TankerTrackers.com believes China is the ultimate destination for the oil on board.

PACIFIC BRAVO is the first major tanker to load Iranian crude after the Trump administration revoked waivers permitting the purchases by eight of Iran’s oil customers. The revocation of the waivers, which sent shockwaves through the global oil market, was a major escalation of Trump’s “maximum pressure” campaign on Iran.

The purchase of Iranian oil in the absence of a waiver exposes the companies involved in the transaction—including the tanker operator, refinery customer, and bank—to possible designation by the U.S. Treasury Department, threatening the links these companies may maintain with the U.S. financial system.

Bank of Kunlun has long been the financial institution at heart of China-Iran bilateral trade—a role for which the company was sanctioned during the Obama administration. Despite already being designated, Bank of Kunlun ceased its Iran-related activities in early May when the oil waivers were revoked. PACIFIC BRAVO’s moves point to a change in policy.

China-Iran trade slowed dramatically after the reimposition of U.S. secondary sanctions in November, suggesting the Chinese government had chosen to subordinate its economic relations with Iran to the much more important issue of its ongoing trade negotiations with the United States. But these negotiations have since broken down. This week, President Trump announced plans to impose tariffs on a further $300 billion in Chinese imports in addition to punitive measures against Chinese telecommunications giant Huawei, which has been targeted in part for its alleged violations of Iran sanctions.

These announcements stoked anger in China, which has vowed to fight back. Last week, foreign ministry spokesman Geng Shuang told reporters that China “resolutely opposes” unilateral sanctions on Iran. But until now, there had been little evidence that the Chinese government was encouraging its companies to ignore or evade U.S. sanctions in the interest of maintaining trade with Iran. While Chinese multinationals will likely remain wary of trading with Iran due to the risks posed to their increasingly global businesses, China’s apparent decision to use state-enterprises to purchase at least some Iranian oil represents a direct and significant challenge to U.S. sanctions. Earlier this week, Trump trade advisor Peter Navarro singled out China’s sanctionable activities in Iran’s metals industry in a Financial Times op-ed. With this kind of messaging, the Trump administration has made it impossible for China to keep the trade war separate from its disagreements with the United States over Iran sanctions.

For Iran, China’s decision to continue to purchase at least some Iranian oil could prove a vital lifeline as it struggles to withstand the Trump administration’s “maximum pressure” sanctions campaign. The failure of Europe, China, and Russia—the remaining parties of the Iran nuclear deal—led Iran to announce last week that it would begin to reduce its compliance with parts of the Joint Comprehensive Plan of Action (JCPOA) in 60 days.

Iran’s announcement greatly concerned European officials who have urged continued compliance with nuclear commitments under the JCPOA. In private, European officials acknowledge that the decision by the Trump administration to revoke the oil waivers was a significant escalation to which Iran was compelled to respond. Noting that economic pressures are fueling political opposition to the JCPOA in Tehran, European officials have been urging Chinese and Russian counterparts to do more to support bilateral economic ties with Iran. Dispatching PACIFIC BRAVO may be just the first step.

Photo: IRNA

Squeezing Gas Prices or Iran? Trump Must Choose

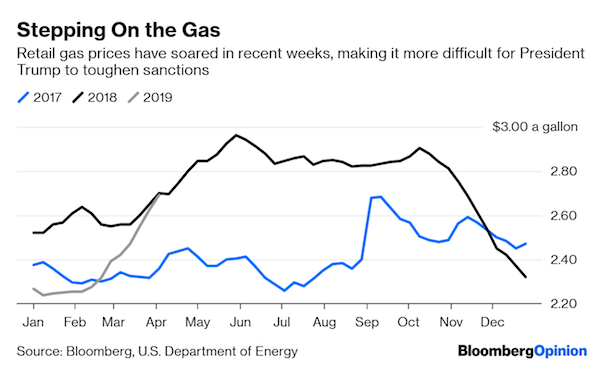

◢ The deadline for the US administration to decide whether to extend sanctions waivers granted to buyers of Iranian oil is now less than a month away, and President Donald Trump faces a tricky decision. He undoubtedly wants to increase pressure on the Persian Gulf nation, but in doing so he risks stoking oil prices and with them those all-important gas prices in swing states back home.

The deadline for the US administration to decide whether to extend sanctions waivers granted to buyers of Iranian oil is now less than a month away, and President Donald Trump faces a tricky decision. He undoubtedly wants to increase pressure on the Persian Gulf nation, but in doing so he risks stoking oil prices and with them those all-important gas prices in swing states back home.

Brian Hook, the US Special Representative for Iran, believes oil market conditions are better this year than they were in 2018 for accelerating the goal of “zeroing out all purchases of Iranian crude,” or so he told reporters last week. But the numbers tell a different story.

That is going to make it more difficult for Trump to go in hard on the remaining buyers of Iran’s oil.

Crude prices have risen nearly 50 percent since Christmas, with WTI popping above USD 62.50 a barrel last week for the first time in almost five months. Retail gasoline prices are on a tear, too. The latest data from the Department of Energy show gas prices up by 18 percent since late February, bringing them back to where they were this time last year.

Meanwhile, in the Persian Gulf, Iran’s visible exports of crude and condensate—a light form of oil produced from gas fields—have been rising steadily since the start of the year. Part of this increase may be due to more of the nation’s oil tankers sending out the radio signals that allow them to be tracked, after much of the fleet turned off transponders to disguise their movements immediately after sanctions were re-imposed. But customs data from importing nations show a similar upward trend.

America’s squeeze on Iran nevertheless allowed some nations to purchase its oil, under a series of six-month-long waivers. These were granted to eight countries, including China, South Korea, Iran, Japan and Turkey, as the restrictions were imposed in November. An estimated 1.76 million barrels a day of crude and condensate left Iran for those five countries in March, up from 1.42 million in February, according to Bloomberg tanker tracking.

This trend contradicts Hook’s assertion that the US is “on the fast track to zeroing out all purchases of Iranian crude.” Three countries that got waivers have cut their purchases to zero, he added. In fact, those three countries—Taiwan, Greece and Italy—haven’t exercised their wavers at all since they were granted. Refiners in Greece and Italy have not received any Iranian cargoes since October, while Taiwan took its last delivery in September.

President Trump’s sanctions have been only slightly tougher than those imposed by his predecessor, despite offering fewer waivers. That will no doubt act as an additional spur for him to heap pressure on the country. But he is going to face difficulties if he wants to get much tougher on Iran next month.

Gas prices remain important to the president and their recent rise must be a source of concern.

The deteriorating situation in two of the “Shaky Six” oil-producing countries I identified a couple of weeks ago is also going to make toughening up the Iran sanctions more difficult.

Venezuela’s oil production is said to have plunged by half during blackouts that rolled across the country last month. Heavy tar-like oil began to solidify in pipelines and tanks after heating systems lost power, causing substantial damage that could take months to fix.

Sanctions imposed on Venezuela’s state oil company have accelerated the output decline, depriving Petroleos de Venezuela of its biggest buyer and the supplier of the light oil it needs to dilute the extra-heavy crude it produces. Output will fall further as the political crisis drags on.

Libya’s production is also at risk again as forces loyal to strongman Khalifa Haftar advance on the capital, Tripoli, threatening a major escalation in violence. Output rose above 1 million barrels a day last month for the first time this year, after the country’s biggest oil field was restarted following a three-month armed occupation. That recovery is now at risk again.

There are two things Trump can do, and his national security team is divided on the course he should follow.

He can allow the unused Iran waivers to expire, claiming a tougher stance without actually affecting oil flows, and perhaps trim the volumes that the remaining countries are permitted to import. Expect particular pressure on Japan and South Korea, who may be more willing than the others to acquiesce to US demands.

He can also continue to lean on Saudi Arabia and the rest of the OPEC+ group to raise output. The Saudis would be very happy to boost production at the expense of their rival, but they will be much less willing than they were last year to do that before seeing Trump actually impose tougher sanctions.

If he has to choose between lower gas prices and tougher Iran sanctions, domestic considerations will probably hold sway. Expect more tweets aimed at Saudi Arabia and OPEC, followed by an extension of five of the eight the waivers, probably permitting reduced volumes of purchases for some, if not all.

Photo Credit: IRNA

Iran Declares Gasoline Self-Sufficiency but Challenges Still Remain

◢ Aiming to achieve self-sufficiency in the production of gasoline, Iran recently launched the third phase of the Persian Gulf Star Refinery, after a massive investment of USD 4 billion. But given rising consumption, the future of genuine gasoline self-sufficiency in Iran might be less bright than the new developments at the Persian Gulf Star suggest.

During a grandiose opening ceremony attended by President Hassan Rouhani and Oil Minister Bijan Zanganeh, Iran inaugurated the third phase of its Persian Gulf Star Refinery in the energy-rich south February 18, declaring "self-sufficiency" in fulfilling national gasoline demand.

Located 25 kilometers west of the port city of Bandar Abbas, the refinery will enable Iran's average daily gasoline production to reach 105 million liters, according to official figures.

The facility, fed by condensate from the South Pars Gas Field in the Persian Gulf, converts light crude into gasoline and other byproducts. The launch of the third phase has been described as a gigantic step in a country whose economy is slowing the face of sanctions reimposed following President Donald Trump's withdrawal from the Joint Comprehensive Plan of Action (JCPOA).

Despite sitting on the world's fourth-largest proved crude oil reserves, Iran has been historically reliant on imports to meet domestic gasoline demand due to insufficient refining capacity.

The latest phase of the Persian Gulf Star Refinery has cost the country USD 4 billion, financed entirely by domestic investment, with no foreign loans secured for the project. While producing 45 million liters of gasoline and 15 million liters of gasoil per day, the refinery also delivers 3 million liters of aviation fuel, as well as 130 tons of sulfur. Iran's oil ministry expects to save USD 15 million per day as imports volumes are expected to fall. The savings are especially important for a government already struggling to supply foreign currency markets amid increasing international banking restrictions.

"Iran's gasoline production has made history with its giant leaps in the past five years," declared Zanganeh during the inauguration ceremony, adding that increased gasoline production would help Iran "to counter unilateral US sanctions".

With the new refinery added to Iran's gasoline production cycle, Iran could feasibly export surplus production. Yet uncertainty related to US sanctions as well as skyrocketing consumption at home in recent years seem to have made the government think twice about export plans. "We have intentionally decided not to export our [surplus] gasoline, because we are planning to maintain good storage,” Zanganeh added without elaborating further.

With Iran's budget largely dependent upon its oil income, experts have for long sounded the alarm on the long-term consequences of the country's single-commodity economy. Consecutive administrations have, therefore, pursued policies to make the economy less reliant on the sale of crude oil. While the goal is yet far from being met, the Rouhani government has focused on diversifying energy exports to include other, higher-value petrol products such as gasoline and gasoil.

"Self-sufficiency in gasoline and gasoil production and moving toward exports were targets set and pursued by the government of Hope and Prudence," reported Arman, a reformist newspaper. In a February 19 editorial, the paper noted that in the face of disruptions caused by the US pullout from the JCPOA, Iran's oil ministry had redoubled efforts toward the self-sufficiency in gasoline production and that more countries besides Iraq and Afghanistan are expected to join the list of Iran's gasoline customers.

The inauguration of the new refinery phase took place just one week after nationwide ceremonies to mark the fortieth anniversary of Iran's Islamic Revolution. State media outlets hailed "gasoline self-sufficiency" as an “achievement and blessing" bestowed by the Islamic Revolution upon the nation. "It came at a time of economic war being waged on our country, with the enemies going the extra mile to inject disappointment in [the minds of] young Iranians," declared a report from the Islamic Republic News Agency (IRNA).

The governor-general of Hormozgan province had earlier described the new refinery as a successful example of Iran’s push to establish a "resistance economy", a term coined by Iran's Supreme Leader Ayatollah Ali Khamenei. The concept has now evolved into a directive to all government institutions, a strategy to neutralize Western measures and a roadmap toward economic independence during sanctions times.

The leading contractor involved in the project was Khatam al-Anbia Construction Headquarters, known by the acronym GHORB. The company is an engineering, procurement, and construction firm with a near monopoly over Iran's mega projects. GHORB is affiliated with Iran's powerful Islamic Revolutionary Guard Corps (IRGC).

Saeed Mohammad, the company’s managing director, told Iran's state TV that the country's share in the enormous South Pars Field now exceeds that of neighboring Qatar. Mohammad also noted that the project was executed by an exclusively Iranian team with an average age of around 30 years old.

But even with the new refining capacity, worries persist that Iran's new gasoline self-sufficiency may be short-lived as domestic consumption continues to rise. The country’s average daily consumption last summer stood at 97 million liters, according to a report by the financial newspaper Donya-e-Eqtesad. Notwithstanding the total capacity of 105 million liters achieved after the inauguration of the third phase, the 9% annual consumption growth rate "will use up the stored gasoline,” the newspaper reports.

Consumption continues to rise because gasoline in Iran remains cheap. Despite rising inflation, Iran's government has in recent years maintained a cap on the price of gasoline. Experts lament the fact that with considerable subsidies allocated to gasoline, the government has not only failed to curb the consumption, but has in fact stoked it. President Rouhani's budget plan for the upcoming Iranian year offers no provision to reduce subsidies in order to reduce consumption.

The future of genuine gasoline self-sufficiency in Iran might be less bright than the development of the Persian Gulf Star Refinery suggests.

Photo Credit: IRNA

Iran Oil Exports: 8 Waivers and the OPEC Meeting

◢ Iran’s oil exports are likely to remain limited in 2019, with significant negative impact on Iran’s economy. Last month, the Trump administration reimposed sanctions on Iran’s energy sector as part of its ‘maximum pressure’ campaign against. But it nevertheless sought to prevent an unhelpful spike in oil prices ahead of the midterm elections. As a result the United States issued eight waivers to importers of Iranian oil:.

This article was originally published by the European Council on Foreign Relations.

Last month, the Trump administration reimposed sanctions on Iran’s energy sector as part of its ‘maximum pressure’ campaign against Iran. But it nevertheless sought to prevent an unhelpful spike in oil prices ahead of the midterm elections. As a result the United States issued eight waivers to importers of Iranian oil: China, India, Japan, South Korea, Turkey, Taiwan, Italy, and Greece. The waivers allow these countries to import a limited amount of oil from Iran without falling foul of US sanctions.

The ‘waiver effect’ was visible from the outset: oil prices dropped the day the waivers were announced. At the same time the market expected other oil producers—particularly Saudi Arabia and Russia—to cut back their temporary production, which had increased over the previous few months to cover Iran’s drop in production. Saudi Arabia and Russia agreed to this at the 7 December OPEC meeting.

The waiver decision initially appeared to be a major setback for the US ‘zero oil’ policy. Yet these eight waivers had a significant impact on the psychology and expectations of the oil market. They have created a perception that there will be an oversupply in the market in the short term, and at least through to the end of 2019.

Now, weeks on from the granting of the waivers, no guidelines or details have been announced publicly with regard to how much these countries will be able to import. This has created confusion in the market as to how much Iran will produce up to April 2019, when the 180-day waiver issued for most of these countries is set to end. Upon the announcement of the waivers, many market analysts had anticipated that Iran’s oil exports would increase to 1.5 million barrels per day (mbpd).

However, the reality could be more complicated. Iran’s oil exports are actually unlikely to increase beyond 1.1 mbpd. At most, they could increase to 1.3 mbpd if market conditions are tight and there is not enough supply in the market. And if China decides to ramp its imports back up to 500,000-560,000 barrels per day (bpd) Iran’s oil exports could increase even further, up to 1.5 mbpd.

Several factors prevent Iran oil exports from increasing significantly over the 180-day period.

China

Under the 2012-15 Obama-era nuclear sanctions, China imported roughly 440,000-530,000 bpd from Iran. However, in October 2018, in light of incoming US sanctions, its imports dropped to about 300,000 b/d. Chinese companies heavily invested in the US are worried and cautious about compliance with the sanctions. China National Petroleum Company—Iran’s largest oil consumer in China—reportedly halted its imports in October and November in order to prevent any potential risk against its business and investment interests in the US. Even though the company announced that it might resume imports from Iran, the market does not expect imports to exceed more than 300,000-360,000 bpd. Adequate market supplies provided by Saudi Arabia’s and Russia’s production mean the Chinese are disinclined to import more ‘problematic’ Iranian oil.

Besides US sanctions exposure for Chinese companies, the ongoing trade negotiations with the US are likely to influence China’s decisions. The US government is granting—on a case-by-case basis—waivers on export tariffs to Chinese companies for their trade with, and exports to, the US. It is likely that major companies and the Chinese government are exercising caution with their oil imports from Iran to avoid other sources of tension with Washington. CNPC has also recently suspended its investment in Iran’s South Pars giant gas field in order to minimise tensions over the trade negotiations. It is noteworthy that Saudi Aramco recently singed five new crude oil supply contracts with China to supply its new refinery capacity in 2019. This will significantly increase Saudi Arabia’s market share in China, reaching a total of about 1.6 mb/d. Saudi Arabia exported an average of about 1 mbpd of oil to China in first 10 months of 2018. This will increase Saudi Arabia’s market share in China by about 11 percent on 2017.

Simply put, China is using its Iran oil imports as part of its tariff negotiations with the US. This is spilling over into China’s own negotiations with Iran. Knowing Iran’s limitations for export, Bejing is bargaining hard and strong with Tehran over prices and delivery conditions. China was very late to issue oil purchase orders to National Iranian Oil Company for the month of November. Chinese refineries waited late – the third week of October—to submit their purchase orders to Iranian authorities.

Limited Shipping Capacity and Payment Issues

Iran’s oil exports have dropped significantly since August 2018 following the implementation of the first round of US secondary sanctions. These put strict limitations on Iran’s oil insurance and shipping. Most of the oil shipped since then has gone through the National Iranian Tanker Company (NITC), even oil shipments to China. Lack of access to adequate insurance has increased the risk of shipping. Most tanker owners are either unwilling to rent their tankers for shipping Iranian oil cargoes or are demanding very high leasing premiums. Hence, importers are mostly relying on NITC to deliver their oil cargoes. This has also impacted on Iran’s refined petroleum products and petrochemical export.

Historically, and in the months since August, NITC’s oil shipments stood at between only 1-1.1 mbpd; this too will prevent Iran from increasing its exports. This is especially the case for Iran’s allocated shipping export capacity to the European Union countries holding waivers (Italy and Greece), as most of its domestic shipping capacity is busy delivering oil to its customers in Asia. Meanwhile, like China, European countries will remain wary of the risks of importing Iranian oil even with the waivers in place.

Sanctions limit Iran’s access to its oil income in the form of cash and hard currency. Due to the latest US sanctions, importers of Iranian oil have to keep Iran’s oil revenues in an escrow account, and Iran can use this credit to purchase certain goods or services. Even for these clients, payment restrictions could also keep oil purchases lower than Tehran hopes. China, India, and Turkey have diverse trade relations with Iran and in theory could pay for Iranian oil with goods such as food and medicine. However, for countries such as Japan and South Korea, paying back Iran’s oil money is complicated. In the case of South Korea, Iran recently signed a food-for-oil agreement. However, there are limitations in terms of volumes and diversity of Iran’s required food from each particular country. Iran has not signed any similar contracts with Japan yet. Auto and electronics industry owners in Asian countries are highly hesitant to barter their products with Iranian oil money, again because they fear losing one of their largest markets: the US.

OPEC

The uncertainty over Iran’s oil exports created a difficult decision-making environment for OPEC members and their non-OPEC allies during their 7 December meeting to finalise a decision over production cuts. This decision aimed to maintain market balance. OPEC and Russia finally agreed to cut their production by 1.2 m/bd, of which OPEC will cut 800,000 b/d and non-OPEC countries (mostly Russia) will cut about 400,000b/d. This volume is in line with Iran’s oil exports of 1.1-1.3 mbpd until the end of the 180-day period. Russian and Saudi Arabian oil production had increased to historic highs in the past few months.

Saudi Arabia in particular came under pressure to reduce its production and generate higher prices, to in turn maintain domestic budget balances. Given the recent warm political, energy, and investment ties between Russia and Saudi Arabia, Russia supported Saudi Arabia’s target for higher oil prices. If not Saudi Arabia’s oil price target of USD 70 per barrel, Russia is supporting at least price range of around USD 60-65 per barrel. Russia also agreed to join OPEC members in a further production cut.

Another significant outcome of this meeting was that Iran was excluded from any production or export cut as its production and export is already below its usual capacity due to the sanctions. In November, Iranian crude oil exports fell slightly below 3 mbpd. The sanctions have not only had a significant impact on Iran crude oil exports, but they have also had a negative impact on Iran’s petroleum product exports. This means that some Iranian refineries are unable to run at full capacity given their export limitations.

A variety of factors are set to impact on the oil market and Iranian oil exports. If the market is adequately supplied and prices remain relatively low, even importers that have received waivers will have little incentive to import oil from Iran. With the prospects of US export capacity rising in 2019 and Saudi Arabia’s and Russia’s own considerable export capacity, Iranian oil exports of 1.1-1.3 mbpd or even less may ensue. If prices remain low countries with waivers may still choose not to import oil from Iran even up to the level for which they received the waivers. Taiwan, Italy, Greece, Turkey, and Japan might behave in this way if they are not convinced that the economic profit of importing Iranian oil is not greater than the risks related to shipping and insuring Iranian oil cargoes. Iran’s oil exports are likely to remain limited in 2019, and so the country’s annual budget for 2019 is based on an export of 1.5 mbpd. This could have a significant negative impact on Iran’s economy—particularly if oil prices remain relatively low throughout 2019.

Photo Credit: IRNA

China Unexpectedly Gambles on European Mechanism to Sustain Iran Trade

◢ China has halted its financial transactions with Iran as part of an unexpected gamble on the future of its trading relationship with the Islamic Republic. According to Majid Reza Hariri, deputy president of the Iran-China Chamber of Commerce, China is hoping to sustain its trade with Iran without putting its financial system in the crosshairs of US authorities by joining the special purpose vehicle being devised by Europe for this purpose.

China has halted its financial transactions with Iran as part of an unexpected gamble on the future of its trading relationship with the Islamic Republic.

Earlier this month, ahead of the reimposition of US sanctions on November 4, China’s Bank of Kunlun informed its clients that it would stop handling all Iran-related payments. The news followed months of speculation that Kunlun, the financial institution at the heart China-Iran trade for more than a decade, would bow to US sanctions pressure.

According to Majid Reza Hariri, deputy president of the Iran-China Chamber of Commerce, China is hoping to sustain its trade with Iran without putting its financial system in the cross hairs of US authorities by joining the special purpose vehicle (SPV) currently being devised in Europe. In the meantime, Chinese trade with Iran has ground to a halt as no banks are available to facilitate transactions.

"It seems that the fate of our trade with China is linked to the support package being prepared by the European Union," Hariri told Bourse & Bazaar in reference to the SPV promised by Iran’s key European trading partners.

The SPV would facilitate trade with Iran by offering a netting service between exporters and importers, reducing the need for funds to be transferred between Iranian banks and foreign financial institutions. Such financial transactions are increasingly difficult due to the risks posed to international banks by US sanctions.

"We are waiting for this financial mechanism to be finalized and for China to join the SPV," Hariri said. In a statement in September, EU High Representative Federica Mogherini stipulated that the SPV “could be opened to other partners in the world.”

Under the previous round of international sanctions, Beijing had designated Kunlun as its primary bank to process billions of dollars payments related to Chinese imports of Iranian oil. The bank also supported the significant growth in non-oil trade between China and Iran as European companies were forced to leave the market when US and EU sanctions came into force.

Kunlun’s perseverance led to US Department of Treasury sanctioning the bank in 2012, but the so-called “bad bank,” shielded by political support from Beijing, continued to maintain its lucrative connections to Iran.

Given this history, the news that Kunlun was cutting-off Iran has served to indicate the intensity of the Treasury Department’s sanctions threats.

Hariri relayed that during his recent trip to China, it became clear that China’s major commercial banks increasingly fear being targeted by US authorities because of links to Kunlun, even if they are not involved in Iran trade themselves.

Bourse & Bazaar also spoke to the chief executive of an Iranian industrial group that conducts significant business with Chinese firms. The executive, who requested anonymity given commercial sensitivities, relayed that large Chinese suppliers do not “want to be in export list, which is where US eyes are looking” because of a pervading fear that “in the weeks following November 4, the US will be making example cases,” targeting companies to create a “system-wide scare.”

Until the situation is better understood, Chinese authorities have opted to pause their trade with Iran and to “let chips fall into place and then figure out way” to sustain commercial ties.

The sudden pause in trade with Iran may explain why China imported an “unprecedented” 20 million barrels of oil to its Dalian refinery in October, twenty times the normal volume. Pointing to issues of energy security, oil analysts do not expect China to cease its imports of Iranian oil, and so the October purchases may have been intended to buy China some time to see if the SPV will become operational.

Two of China’s leading refiners, Sinopec Group and China National Petroleum Corporation, the parent company of Bank of Kunlun, have not placed any orders to purchase Iranian oil in November.

Reports suggest that the SPV will be legally established on or around the November 4 sanctions deadline, but it may take several months for operations to begin in earnest. There remain many hurdles. EU member states are understandably less than enthusiastic about the prospect of hosting the financial channel that will be perceived by US authorities as an attempt to circumvent sanctions.

If SPV fails to become operational or is unable to accept Chinese participation, it will fall to China and Iran to find a new bilateral banking channel, explained Hariri. "If the EU continues with its procrastination, we can once more restart efforts to continue bilateral banking relations," he said.

It is unclear what a new financial channel look like. On Monday, Iranian reports cited "credible sources" to claim that Beijing aims to establish "a new banking mechanism" to continue working with Iran and several meetings have already been held on the matter.

Iran may seek to hold an ownership stake in the new banking channel. The concept that Iranians could become shareholders in Chinese banks has been floated for about a decade. But new draft rules issued by the Chinese regulators may present Iran with a new window of opportunity. Regulators now allow foreign entities to set up wholly owned banks and branches in China.

As Hariri points out, any negotiations over the Chinese participation in the SPV or the creation of a new banking channel are made more complicated by the fact that Iran currently lacks an ambassador to Beijing. Nonetheless, it seems likely that sooner or later Iran-China trade will resume, even under US sanctions. Iran is too lucrative a market for China to simply ignore.

The question is how long Iran’s business community can wait for the rebound. While Iran may have sold a bumper volume of oil in October, private sector companies were caught off guard by China’s move to halt trade. In a matter of weeks, inventories of manufacturing inputs and finished goods will begin to run out.

Photo Credit: Xinhua

Iran’s Oil Exports May Be More Resilient Than Headlines Suggest