Iran's Oil Sector is Breaking Out

Iran’s oil exports are rising and the sector is growing for the first time in two years. The recovery poses a dilemma for Biden, who faces a growing constituency in Tehran unsure if there's enough to be gained should the US be allowed to rejoin the JCPOA.

In August 2019, Mike Pompeo took something of a victory lap. Speaking to MSNBC, he declared that the Trump administration had “managed to take almost 2.7 million barrels of [Iranian] crude oil off of the market.” A few months prior, the United States had reimposed secondary sanctions on Iran’s oil sector, revoking eight waivers that allowed Iran’s major oil customers to temporarily continue purchasing Iranian oil. Without the waivers, just one major buyer remained—China. At the time of Pompeo’s boast, China was buying a negligible volume of Iranian oil in direct violation of US sanctions. Beijing protested loudly about the extraterritorial impact of US sanctions, but proved unable or unwilling to instruct its major refiners, banks, and tanker companies to sustain the previous level of imports from Iran.

In Tehran, the loss of oil revenues was adding to the political and fiscal pressures felt by the Rouhani administration, already reeling from the economic fallout following Trump’s withdrawal from the Joint Comprehensive Plan of Action (JCPOA). Iran’s oil minister, Bijan Zanganeh, vowed in October 2019 to “use every possible way” to sustain Iran’s oil exports. In the subsequent year, Iran made its tankers “go dark,” engaged in ship-to-ship transfers off the coast of the UAE and Malaysia to hide the provenance of its oil, sold to opportunistic new customers including Syria and Venezuela, and intensively lobbied China to resume purchases at higher volumes.

Today it is Zanganeh who is taking a victory lap. He told reporters last week that Iran’s oil exports are “much better than many assume,” and the oil ministry has announced that it would begin ramping-up oil production. Data from TankerTrackers.com, which observes the number of tankers leaving Iran’s ports in order to estimate oil exports, suggests a steady uptick in sales. January 2021 will be the fifth month in a row that Iran has exported in excess of 1 million barrels per day of crude oil and condensates. The new monthly level marks a significant increase from the average of 695,000 barrels per day Iran managed in the 12 months following the Trump administration’s revocation of the oil waivers.

Should the Iranian oil industry recover in the first half of 2021, buoyed by the rise in oil prices from their pandemic lows, the sector would cease to be the deadweight holding Iran’s economy back. The second quarter of this Iranian calendar year marked the first in over two years in which Iran’s oil and gas sector was not in contraction. The International Monetary Fund, the World Bank, and the Institute for International Finance all project Iran’s economy to return to growth in 2021 on the basis of conservative projections for oil production and exports achieved in the absence of sanctions relief. Iran appears poised to match those projections.

Iran’s rising oil exports pose a dilemma for President Joe Biden, who intends to bring the US back into the nuclear deal. There is a significant political constituency in Tehran that believes that allowing the US to rejoin the JCPOA would be a strategic mistake. The Biden administration has signalled that JCPOA re-entry would serve as the foundation for follow-on talks, a prospect that has Iranian hardliners concerned that the international community will try to force Iran into making painful concessions on strategic issues such as the country’s ballistic missile program.

The Rouhani administration remains strongly in favor of renewed talks and has indicated that it would welcome reentry into the JCPOA should the Biden administration decisively lift the sanctions imposed by Trump and thereby deliver Iran an economic uplift. But the attractiveness of Rouhani’s preferred approach depends entirely on the perceived opportunity cost should Iran fail to engage in new talks. This cost appears to be shrinking as Iran’s economic recovery picks-up steam and as the ferocity of political opposition Biden faces on the JCPOA becomes clear. Iran’s Supreme Leader, Ali Khamenei, presented “defusing sanctions and overcoming them” as the preferred alternative to Rouhani’s efforts for “lifting sanctions” in a important speech last November—a nod to the growing doubts that negotiations are necessary in the short-term.

For now, Iran’s political establishment remains open to negotiations because the country would be entering new talks from a position of relative strength. But that same strength will enable Iran’s hardliners to close the door on diplomacy should Biden dither.

Biden may be tempted to address the dilemma he faces be reasserting economic leverage. But attempting to drive down the oil exports with further sanctions would be a mistake. The only measures that might serve to stop China’s purchases of Iranian crude would require designations on China’s state-owned refiners such as Sinopec and CNPC, subsidiaries of which are widely represented in the portfolios of American and European institutional investors. Such a move would not only risk triggering a true economic war with China, but it would also cause a significant disruption to energy and financial markets.

Moreover, the risks of Iranian retaliation remain high. Iranian leaders have consistently warned that it would seek to deny oil exports by neighbors should it be prevented from selling its own oil. The September 2019 cruise missile attacks on Saudi Aramco’s Abqaiq and Khurrais facilities, which caused production capacity to drop by half, serves as an example of the very real nature of that threat.

Clearly, Biden has no easy means to bring Iranian exports back down. So long as China continues buying, Iranian persistence will ensure the barrels reach the buyers. A few more months of sustained recovery in exports may be enough to convince Iran’s ascendent hardliners that the country’s economic outlook under sanctions is no longer so negative as to be a political or practical liability, meaning their opposition to the JCPOA will carry no real cost. Biden needs to move fast if he is to save the basic quid-pro-quo that underpins the nuclear deal.

To do so, Biden must take steps to widen the opportunity cost between diplomacy and defiance once again. His administration ought to immediately issue new, temporary oil waivers in order to enable Iran to export oil without directly contravening US sanctions. Such a move would benefit US allies such as Italy, South Korea, Japan, and India, which count among Iran’s historical oil customers—US sanctions policy would no longer be at odds with their energy security.

The waivers would also help de-escalate tensions with China enabling cooperation on the creation of a stronger non-proliferation framework for the Middle East. The Trump administration used Iran sanctions as a means to target major Chinese enterprises including telecommunications firms Huawei and ZTE and shipping giant COSCO. These designations and the systemic threat their proliferation posed to the Chinese economy have spurred Chinese authorities to begin development of an alternative to the SWIFT bank messaging system and to instruct state lenders to prepare contingencies for further US sanctions pressure. Similar measures have even been contemplated by European governments. These moves foreshadow how the overuse of US sanctions threatens their long-term efficacy. Issuing new oil waivers would see Biden remove the primary impetus for these mitigation efforts in China and other countries.

Restoring the waivers would also be welcomed by Iran, which could expect to see oil exports double, rising above the level possible through the complex and expensive methods of sanctions evasion currently in use. The additional foreign exchange revenue afforded by the waivers would help Iran more fully address its balance of payments crisis, easing pressure on the country’s currency and thereby reducing the rampant inflation that has led to hardship for millions of Iranians. The Biden administration can be confident that the additional revenues would have this effect because of the restrictions in place around their use. The waiver system, first designed during the Obama administration, sees revenues accrue in escrow accounts carefully monitored by authorities in the countries which have been granted the waivers. This oversight ensures that the funds are used for the purchase of sanctions-exempt goods and not for what the Trump administration termed “malign activities.” The funds cannot be transferred to Iran nor any third country without specific approvals.

Despite these restrictions, for Iranian stakeholders, the issuing of new waivers would represent an important gesture, indicating Biden’s seriousness about restoring the economic benefits originally envisioned under the JCPOA, and setting the stage for US-Iran talks on the sequencing of steps to restore mutual compliance with the nuclear deal. Should those talks fail, Biden would surely revoke the waivers and Iran would return to selling oil in defiance of US sanctions. But should the talks succeed, the early provision of the waivers will have served to accelerate the reestablishment of Iran’s sales to oil customers, helping the country win back coveted market share.

Iran’s oil industry is breaking out. Issuing new oil waivers is the best way to ensure Iran ceases to seek leverage by reducing its compliance with the nuclear deal and begins to believe again in the potential for “win-win” diplomacy with the United States.

Biden needs to give up some pressure in order to gain back control.

Photo: SHANA

Squeezing Gas Prices or Iran? Trump Must Choose

◢ The deadline for the US administration to decide whether to extend sanctions waivers granted to buyers of Iranian oil is now less than a month away, and President Donald Trump faces a tricky decision. He undoubtedly wants to increase pressure on the Persian Gulf nation, but in doing so he risks stoking oil prices and with them those all-important gas prices in swing states back home.

The deadline for the US administration to decide whether to extend sanctions waivers granted to buyers of Iranian oil is now less than a month away, and President Donald Trump faces a tricky decision. He undoubtedly wants to increase pressure on the Persian Gulf nation, but in doing so he risks stoking oil prices and with them those all-important gas prices in swing states back home.

Brian Hook, the US Special Representative for Iran, believes oil market conditions are better this year than they were in 2018 for accelerating the goal of “zeroing out all purchases of Iranian crude,” or so he told reporters last week. But the numbers tell a different story.

That is going to make it more difficult for Trump to go in hard on the remaining buyers of Iran’s oil.

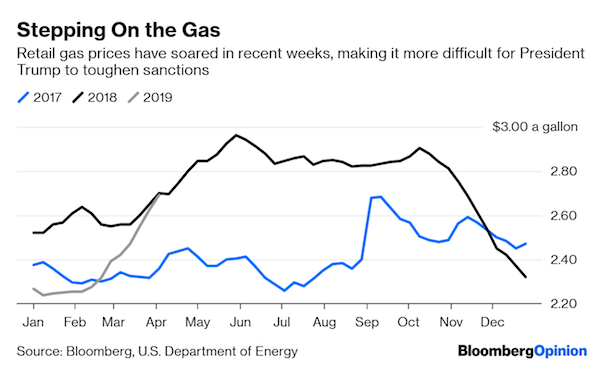

Crude prices have risen nearly 50 percent since Christmas, with WTI popping above USD 62.50 a barrel last week for the first time in almost five months. Retail gasoline prices are on a tear, too. The latest data from the Department of Energy show gas prices up by 18 percent since late February, bringing them back to where they were this time last year.

Meanwhile, in the Persian Gulf, Iran’s visible exports of crude and condensate—a light form of oil produced from gas fields—have been rising steadily since the start of the year. Part of this increase may be due to more of the nation’s oil tankers sending out the radio signals that allow them to be tracked, after much of the fleet turned off transponders to disguise their movements immediately after sanctions were re-imposed. But customs data from importing nations show a similar upward trend.

America’s squeeze on Iran nevertheless allowed some nations to purchase its oil, under a series of six-month-long waivers. These were granted to eight countries, including China, South Korea, Iran, Japan and Turkey, as the restrictions were imposed in November. An estimated 1.76 million barrels a day of crude and condensate left Iran for those five countries in March, up from 1.42 million in February, according to Bloomberg tanker tracking.

This trend contradicts Hook’s assertion that the US is “on the fast track to zeroing out all purchases of Iranian crude.” Three countries that got waivers have cut their purchases to zero, he added. In fact, those three countries—Taiwan, Greece and Italy—haven’t exercised their wavers at all since they were granted. Refiners in Greece and Italy have not received any Iranian cargoes since October, while Taiwan took its last delivery in September.

President Trump’s sanctions have been only slightly tougher than those imposed by his predecessor, despite offering fewer waivers. That will no doubt act as an additional spur for him to heap pressure on the country. But he is going to face difficulties if he wants to get much tougher on Iran next month.

Gas prices remain important to the president and their recent rise must be a source of concern.

The deteriorating situation in two of the “Shaky Six” oil-producing countries I identified a couple of weeks ago is also going to make toughening up the Iran sanctions more difficult.

Venezuela’s oil production is said to have plunged by half during blackouts that rolled across the country last month. Heavy tar-like oil began to solidify in pipelines and tanks after heating systems lost power, causing substantial damage that could take months to fix.

Sanctions imposed on Venezuela’s state oil company have accelerated the output decline, depriving Petroleos de Venezuela of its biggest buyer and the supplier of the light oil it needs to dilute the extra-heavy crude it produces. Output will fall further as the political crisis drags on.

Libya’s production is also at risk again as forces loyal to strongman Khalifa Haftar advance on the capital, Tripoli, threatening a major escalation in violence. Output rose above 1 million barrels a day last month for the first time this year, after the country’s biggest oil field was restarted following a three-month armed occupation. That recovery is now at risk again.

There are two things Trump can do, and his national security team is divided on the course he should follow.

He can allow the unused Iran waivers to expire, claiming a tougher stance without actually affecting oil flows, and perhaps trim the volumes that the remaining countries are permitted to import. Expect particular pressure on Japan and South Korea, who may be more willing than the others to acquiesce to US demands.

He can also continue to lean on Saudi Arabia and the rest of the OPEC+ group to raise output. The Saudis would be very happy to boost production at the expense of their rival, but they will be much less willing than they were last year to do that before seeing Trump actually impose tougher sanctions.

If he has to choose between lower gas prices and tougher Iran sanctions, domestic considerations will probably hold sway. Expect more tweets aimed at Saudi Arabia and OPEC, followed by an extension of five of the eight the waivers, probably permitting reduced volumes of purchases for some, if not all.

Photo Credit: IRNA

Iran Oil Exports: 8 Waivers and the OPEC Meeting

◢ Iran’s oil exports are likely to remain limited in 2019, with significant negative impact on Iran’s economy. Last month, the Trump administration reimposed sanctions on Iran’s energy sector as part of its ‘maximum pressure’ campaign against. But it nevertheless sought to prevent an unhelpful spike in oil prices ahead of the midterm elections. As a result the United States issued eight waivers to importers of Iranian oil:.

This article was originally published by the European Council on Foreign Relations.

Last month, the Trump administration reimposed sanctions on Iran’s energy sector as part of its ‘maximum pressure’ campaign against Iran. But it nevertheless sought to prevent an unhelpful spike in oil prices ahead of the midterm elections. As a result the United States issued eight waivers to importers of Iranian oil: China, India, Japan, South Korea, Turkey, Taiwan, Italy, and Greece. The waivers allow these countries to import a limited amount of oil from Iran without falling foul of US sanctions.

The ‘waiver effect’ was visible from the outset: oil prices dropped the day the waivers were announced. At the same time the market expected other oil producers—particularly Saudi Arabia and Russia—to cut back their temporary production, which had increased over the previous few months to cover Iran’s drop in production. Saudi Arabia and Russia agreed to this at the 7 December OPEC meeting.

The waiver decision initially appeared to be a major setback for the US ‘zero oil’ policy. Yet these eight waivers had a significant impact on the psychology and expectations of the oil market. They have created a perception that there will be an oversupply in the market in the short term, and at least through to the end of 2019.

Now, weeks on from the granting of the waivers, no guidelines or details have been announced publicly with regard to how much these countries will be able to import. This has created confusion in the market as to how much Iran will produce up to April 2019, when the 180-day waiver issued for most of these countries is set to end. Upon the announcement of the waivers, many market analysts had anticipated that Iran’s oil exports would increase to 1.5 million barrels per day (mbpd).

However, the reality could be more complicated. Iran’s oil exports are actually unlikely to increase beyond 1.1 mbpd. At most, they could increase to 1.3 mbpd if market conditions are tight and there is not enough supply in the market. And if China decides to ramp its imports back up to 500,000-560,000 barrels per day (bpd) Iran’s oil exports could increase even further, up to 1.5 mbpd.

Several factors prevent Iran oil exports from increasing significantly over the 180-day period.

China

Under the 2012-15 Obama-era nuclear sanctions, China imported roughly 440,000-530,000 bpd from Iran. However, in October 2018, in light of incoming US sanctions, its imports dropped to about 300,000 b/d. Chinese companies heavily invested in the US are worried and cautious about compliance with the sanctions. China National Petroleum Company—Iran’s largest oil consumer in China—reportedly halted its imports in October and November in order to prevent any potential risk against its business and investment interests in the US. Even though the company announced that it might resume imports from Iran, the market does not expect imports to exceed more than 300,000-360,000 bpd. Adequate market supplies provided by Saudi Arabia’s and Russia’s production mean the Chinese are disinclined to import more ‘problematic’ Iranian oil.

Besides US sanctions exposure for Chinese companies, the ongoing trade negotiations with the US are likely to influence China’s decisions. The US government is granting—on a case-by-case basis—waivers on export tariffs to Chinese companies for their trade with, and exports to, the US. It is likely that major companies and the Chinese government are exercising caution with their oil imports from Iran to avoid other sources of tension with Washington. CNPC has also recently suspended its investment in Iran’s South Pars giant gas field in order to minimise tensions over the trade negotiations. It is noteworthy that Saudi Aramco recently singed five new crude oil supply contracts with China to supply its new refinery capacity in 2019. This will significantly increase Saudi Arabia’s market share in China, reaching a total of about 1.6 mb/d. Saudi Arabia exported an average of about 1 mbpd of oil to China in first 10 months of 2018. This will increase Saudi Arabia’s market share in China by about 11 percent on 2017.

Simply put, China is using its Iran oil imports as part of its tariff negotiations with the US. This is spilling over into China’s own negotiations with Iran. Knowing Iran’s limitations for export, Bejing is bargaining hard and strong with Tehran over prices and delivery conditions. China was very late to issue oil purchase orders to National Iranian Oil Company for the month of November. Chinese refineries waited late – the third week of October—to submit their purchase orders to Iranian authorities.

Limited Shipping Capacity and Payment Issues

Iran’s oil exports have dropped significantly since August 2018 following the implementation of the first round of US secondary sanctions. These put strict limitations on Iran’s oil insurance and shipping. Most of the oil shipped since then has gone through the National Iranian Tanker Company (NITC), even oil shipments to China. Lack of access to adequate insurance has increased the risk of shipping. Most tanker owners are either unwilling to rent their tankers for shipping Iranian oil cargoes or are demanding very high leasing premiums. Hence, importers are mostly relying on NITC to deliver their oil cargoes. This has also impacted on Iran’s refined petroleum products and petrochemical export.

Historically, and in the months since August, NITC’s oil shipments stood at between only 1-1.1 mbpd; this too will prevent Iran from increasing its exports. This is especially the case for Iran’s allocated shipping export capacity to the European Union countries holding waivers (Italy and Greece), as most of its domestic shipping capacity is busy delivering oil to its customers in Asia. Meanwhile, like China, European countries will remain wary of the risks of importing Iranian oil even with the waivers in place.

Sanctions limit Iran’s access to its oil income in the form of cash and hard currency. Due to the latest US sanctions, importers of Iranian oil have to keep Iran’s oil revenues in an escrow account, and Iran can use this credit to purchase certain goods or services. Even for these clients, payment restrictions could also keep oil purchases lower than Tehran hopes. China, India, and Turkey have diverse trade relations with Iran and in theory could pay for Iranian oil with goods such as food and medicine. However, for countries such as Japan and South Korea, paying back Iran’s oil money is complicated. In the case of South Korea, Iran recently signed a food-for-oil agreement. However, there are limitations in terms of volumes and diversity of Iran’s required food from each particular country. Iran has not signed any similar contracts with Japan yet. Auto and electronics industry owners in Asian countries are highly hesitant to barter their products with Iranian oil money, again because they fear losing one of their largest markets: the US.

OPEC

The uncertainty over Iran’s oil exports created a difficult decision-making environment for OPEC members and their non-OPEC allies during their 7 December meeting to finalise a decision over production cuts. This decision aimed to maintain market balance. OPEC and Russia finally agreed to cut their production by 1.2 m/bd, of which OPEC will cut 800,000 b/d and non-OPEC countries (mostly Russia) will cut about 400,000b/d. This volume is in line with Iran’s oil exports of 1.1-1.3 mbpd until the end of the 180-day period. Russian and Saudi Arabian oil production had increased to historic highs in the past few months.

Saudi Arabia in particular came under pressure to reduce its production and generate higher prices, to in turn maintain domestic budget balances. Given the recent warm political, energy, and investment ties between Russia and Saudi Arabia, Russia supported Saudi Arabia’s target for higher oil prices. If not Saudi Arabia’s oil price target of USD 70 per barrel, Russia is supporting at least price range of around USD 60-65 per barrel. Russia also agreed to join OPEC members in a further production cut.

Another significant outcome of this meeting was that Iran was excluded from any production or export cut as its production and export is already below its usual capacity due to the sanctions. In November, Iranian crude oil exports fell slightly below 3 mbpd. The sanctions have not only had a significant impact on Iran crude oil exports, but they have also had a negative impact on Iran’s petroleum product exports. This means that some Iranian refineries are unable to run at full capacity given their export limitations.

A variety of factors are set to impact on the oil market and Iranian oil exports. If the market is adequately supplied and prices remain relatively low, even importers that have received waivers will have little incentive to import oil from Iran. With the prospects of US export capacity rising in 2019 and Saudi Arabia’s and Russia’s own considerable export capacity, Iranian oil exports of 1.1-1.3 mbpd or even less may ensue. If prices remain low countries with waivers may still choose not to import oil from Iran even up to the level for which they received the waivers. Taiwan, Italy, Greece, Turkey, and Japan might behave in this way if they are not convinced that the economic profit of importing Iranian oil is not greater than the risks related to shipping and insuring Iranian oil cargoes. Iran’s oil exports are likely to remain limited in 2019, and so the country’s annual budget for 2019 is based on an export of 1.5 mbpd. This could have a significant negative impact on Iran’s economy—particularly if oil prices remain relatively low throughout 2019.

Photo Credit: IRNA